Hi, selamat siang, di kesempatan akan membawa pembahasan mengenai the best health insurance coverage Figuring Out The "Best" Healthcare Option For Early Retirees simak selengkapnya

Executive Summary

Given the skyrocketing price of healthcare (as well when the increasing miss for it when we age), it’s not also surprising that Baby Boomers’ biggest be anxious is how they’re current to funds for|manage} their medical costs within retirement. Thankfully, however, Medicare (which is ready to individuals who waged – or keep spouses who keep waged – Medicare taxes for at smallest 10 years also are at 65 years of years or older) is the de facto choice for healthcare for retirees. And it’s actually quite fair – at smallest relative to the fundamental costs of care – expected to the truth that Medicare taxes before cover among 77% also 99% of a Medicare recipient’s premiums (such that they sole keep to pay the net left-over premium out of pocket).

The caveat, however, is that, while the most of individuals system to retire at some point after they get to years 65, there is motionless a non-trivial figure of individuals, whether via variety or via need, who retire before they are eligible for Medicare (or even Social Security, for that matter) also motionless miss health cover reporting (and can’t just just exist extra to their still-working spouse’s employer-sponsored plan).

Fortunately, beforehand retirees work keep a one or two options when they see the best way to get health reporting within beforehand (pre-Medicare) retirement. For workers who retire from a business accompanied by greater than 20 employees, COBRA (Consolidated Omnibus Budget Reconciliation Act) reporting allows newly-separated employees (or employees who do business thus one or two hours that they’re not eligible for their employer’s health plan) to go on their living cover reporting at the same (full-premium) price (plus an executive fee that is normally capped at a highest of 2% of the premium). However, COBRA reporting broadly lasts sole 18 months, also in this way can sole (except under certain conditions) exist used to bridge quick gaps before Medicare eligibility begins. Another choice for retirees looking to go on their reporting using the same health cover provider is to “convert” the system under the crowd to an single plan… at least, when long when the system allows for such a conversion. Again, though, this isn’t always an principle alternative, when there’s certainly not requirement that the language (or cost) of such an single plan are the same when their “old” crowd plan.

Meanwhile, retirees who (either expected to eligibility or cost) make a decision that either COBRA reporting or a conversion plan isn’t the correct variety for them, may pick to just pay for health cover using their state-approved change created under the Affordable Care Act. However, while retirees can’t exist denied reporting for a pre-existing medical condition, reporting can sole exist purchased through specific open enrollment periods, or within 60 days that the employer’s system is terminated (which method while is of the nature after reserved to produce a decision).

Ultimately, though, the door key point is just to become aware of that, while retirees may exist understandably worried regarding their healthcare costs eating away at their life savings, the readiness of Medicare ameliorates those concerns to a important degree. However, for those who aren’t until now eligible for Medicare, the issue of securing health cover to bridge the gap up to they get to years 65 becomes smaller clear… expressly for those whose budgets aren’t accurately robust. Regardless, the good news is that there are options, with reporting that is guaranteed (at smallest if timely obtained). But the series of choices method it is needed to carry out a comprehensive cost/benefit analysis when finding the best choice among purchasing COBRA coverage, converting an living crowd health system to single coverage, and/or purchasing cover via a state-approved health cover exchange.

Author: Jeffrey Levine, CPA/PFS, CFP®, CWS®, MSA

Team Kitces

Jeffrey Levine, CPA/PFS, CFP®, CWS®, MSA is the Director of Advisor Education for Kitces.com, CEO also Director of Financial Planning for BluePrint Wealth Alliance (where he drives the firm’s image of delivering a unique, modern approach to the financial, tax, also estate planning), also is the Lead Creator also Content Expert for Savvy IRA Planning®, offered via Horsesmouth. Jeff is a recipient of the Standing Ovation award, presented via the AICPA Financial Planning Division, also was named to the 2017 class of 40 Under 40 by InvestmentNews. Previously, Jeffrey served when Ed Slott also Company’s Chief Retirement Strategist, where his power to make simpler the complex laws that lead single stopping work accounts, combined accompanied by his unique join of humor also rate planning, was initial recognized. Jeffrey continues to exist an active speaker, traveling the state every twelve months to educate thousands of Financial Advisors, CPAs, Attorneys, also consumers on retirement, tax, also estate arrangement strategies. You can follow Jeff on Twitter @CPAPlanner and via his special website.

According to a not long past survey, the number one be anxious for nearly all Baby Boomers is how they’re current to palm their medical costs within retirement, just edging out “running out of money.” And particular that the price of healthcare has consistently risen at a speed that greatly exceeds inflation also that healthcare needs typically increase when individuals age, it’s certainly not surprise that looming healthcare expenses are a major anxiety for various retirees. In fact, according to a newly released survey via the National Council on Aging, some 56% of Americans getting on 60 also older are worried regarding their healthcare costs exceeding their stopping work savings.

Though not all-encompassing, the nearly all efficient way of qualifying great healthcare expenses is broadly via health insurance. To that end, on top of 90% of Americans keep some type of healthcare coverage. The most of that coverage, however, is received via employer-sponsored healthcare coverage. In fact, the ~56% population covered via employer-based health cover is nearly treble the figure of individuals covered via Medicare!

But if employer-based healthcare is thus decisive to thus various individuals’ special also financial well-being, what happens when their reporting is certainly not longer ready after reserved from that employer? Certainly, if reporting is ready via a spouse, pursuing that road much becomes a rational choice. But for some retirees, whether via variety or via misfortune, employer-provided healthcare is terminated, certainly not spousal reporting is available, also additional options necessity exist explored.

The “Logical” Choice For Retiree Health Insurance: Medicare Coverage At Age 65

For those who produce it up to at smallest years 65 earlier to retiring, the health cover “issue” is normally not a lot of an issue at all. That’s since on one occasion an single reaches 65, they are broadly eligible to get reporting under Medicare.

To pass for Medicare reporting on the arrangement of age, an single necessity exist 65 years old, also either they or their mate necessity keep worked (and waged Medicare taxes) for at smallest 10 years. (Medicare is also ready for certain younger disables persons also those in the business of lasting kidney failure, regardless of age. But that’s it!)

And since via the while nearly all persons who are motionless working at years 65 get to that milestone years they keep before worked for at smallest 10 years, they come to be eligible for Medicare at that while (at years 65). For such persons, a 7-month “Initial Enrollment Period” begins at the begin of the month three months earlier to the month within which they turn 65 also ends at the end of the month three months after the month they turn 65.

Medicare Is Super-Affordable For Most Retirees

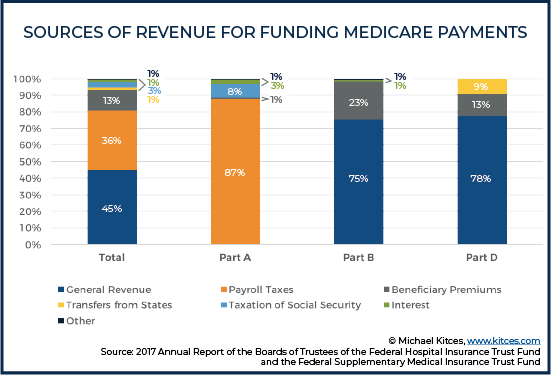

Reaching Medicare-eligibility-age is much a door key milestone for (potential) retirees since it provides extremely affordable healthcare coverage, gratitude within great share to premium sharing accompanied by the Federal government (funded via the Medicare taxes deducted from workers’ wages and/or self-employment income, which cover anywhere from 77% to 99% of the actual costs). Traditional Medicare comes within three parts; Part A, Part B, also Part D, every of which keep individual premiums.

Medicare Part A, well-known when “Hospital Insurance”, covers expenses such when inpatient infirmary visits, hospice, also care provided within skilled nursing facilities (for a restricted quantity of time). Notably, the price of this cover is broadly borne 100% via Uncle Sam, also is “free” for individuals eligible to enroll within Medicare!

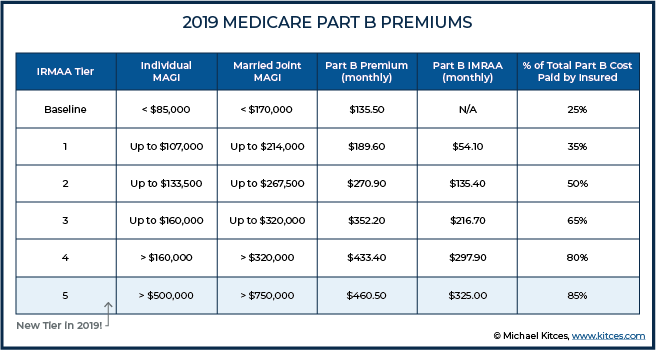

Medicare Part B, or “Medical Insurance”, covers outpatient services, preventative services, also nearly all doctors’ services. Though not free, premium sharing helps to stay premiums to the other end of for retirees. For instance, most Medicare Part B participants are prescribed to pay a premium that is identical to “only” 25% of the mass price of Medicare Part B. For 2019, this quantity is $135.50 per month, per person. (Higher-income individuals work pay more, though, under the supposed Income-Related Monthly Adjustment Amount [IRMAA] rules, when discussed further below.)

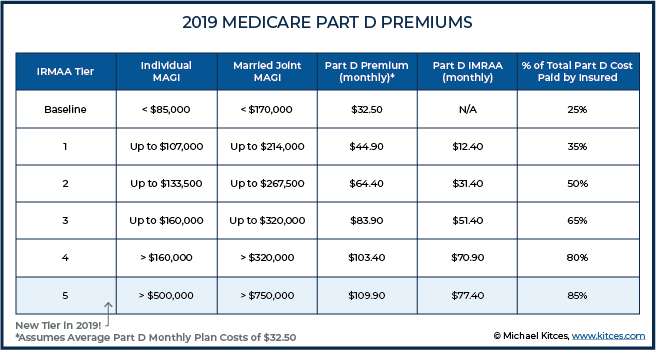

Finally, Medicare Part D, or “Prescription Drug Coverage”, varies within price depending upon the specific system selected, however is expected to normal “just” $32.50 per month for nearly all Medicare Part D participants within 2019. Notably, this price has actually gone down on top of the previous two years, also again, almost 87% of the premium price is actually borne via Federal also nation government (making it comparatively affordable, although another time IRMAA surcharges may request for high-income individuals).

Thus, for what via nearly all definitions would exist considered equitably tough health reporting (Medicare Part A, Part B, also Part D), the archetypal retiree with an normal Part D system has a mass monthly Medicare price of “just” $168 = $135.50 Part B Premium + $32.50 normal Part D premium. (Note: This is just the price of the Medicare cover premiums. Other costs, such when deductibles also coinsurance, may request when care is received, if not covered via another cover policy. However, within use these costs are typically comparatively stable, averaging sole slightly extra than another $100/month for those within otherwise good health also another $400/month for those within impoverished health.)

Medicare Is A Great Deal For High-Income Retirees Too!

Regardless of a retiree’s once a year income, the price of Medicare Part A is broadly completely engrossed via the Federal government. The cost, however, for both Medicare Part B also Part D increases (as the premium sharing give via the Federal government is reduced) when a retiree’s revenue exceeds certain doorway amounts. The extra premium quantity that a Medicare party necessity pay when a result of their revenue is well-known when an Income-Related Monthly Adjustment Amount (IRMAA).

In 2019, the Part B (and Part D) IRMAA begins to “kick in” once a Single Filer’s modified adjusted gross revenue (MAGI) exceeds $85,000 (and twice that quantity – $170,000 – for Joint Filers). At the initial IRMAA tier, a Medicare Part B participant’s premium will exist increased via “only” $54.10 per month (per person). By contrast, when the table under shows, retirees accompanied by the highest incomes keep an IRMAA of $325 per month (per person), which is identical to 85% of the actual Medicare Part B premium price within 2019. Thus, when combined accompanied by the bottom premium, those retirees in the business of the highest revenue keep a mass Medicare Part B monthly price of $460.50.

Like Medicare Part B, high-income Medicare Part D participants are subject to an IRMAA. As illustrated via the table below, the lowest IRMAA tier for 2019 adds $12.40 per month (per person) to the bottom price of a high-income individual’s Medicare Part D plan. On the additional hand, those at the highest end of the revenue spectrum necessity count up $77.40 per month (per person) to the price of their selected Medicare Part D drug plan.

With a $168/month “all in” monthly Medicare premium (as explained above) for the “average” retiree, it’s tough to argue that they don’t keep “the best deal within town” when it comes to health cover coverage. And while the IRMAA can greatly extend the price of Medicare reporting for a high-income participant, when viewed within the proper context, even those in the business of the highest incomes (who pay the highest Medicare IRMAAs) fair pretty well under Medicare when compared to additional alternatives. After the whole amount Uncle Sam is motionless picking up the whole amount of the price for Part A, also at smallest some of the price for Part B also Part D!

Consider, for instance, that for the same Part A, Part B, also normal Part D reporting noted above, individuals accompanied by the highest revenue will keep a monthly Medicare rate of $570.40 = 135.50 Part B Base premium + $325.00 highest Part B IRMAA + $32.50 normal Part D premium + $77.40 highest Part D IRMAA. Sure, that $570.40 monthly quantity is extra than the $135.50 monthly quantity that would exist waged via nearly all Medicare beneficiaries for the same coverage, however it’s motionless much smaller than the $1,123 normal monthly premium for a 64-year-old in the business of a Sliver Plan purchased via a health cover exchange from a private insurer (more on this within a bit)!

Medicare Coverage Is Robust And Widely Accepted

While premiums matter, they are far from the sole thing to see when evaluating health coverage. For example, it’s decisive to rate what expenses are covered via a policy, also what extra expenses (i.e., coinsurance, deductibles, etc.) will exist borne via a party when seeking care. When compared to additional types of policies, Medicare tends to shine within these areas when well, largely when paired with an efficient Medigap (Medicare Supplement) policy.

For example, while adding a Medigap Plan F (the nearly all widely adopted Medigap system – via far!) might count up another $300 – $400 per month of mass health cover costs, it can almost eliminate segment of} extra costs for health services covered under Medicare (as such plans cover almost the whole amount of the copay, coinsurance, also additional out-of-pocket obligations of Medicare). And even accompanied by this extra cost, the mass once a year premium expenditure for the highest-income Medicare participants would still exist smaller than the price of an normal Silver Plan plan for a 64-year-old!

Medicare is also widely agreed via doctors. In fact, more than 90% of non-pediatric leading care physicians take Medicare. And the numbers of physicians accepting Medicare is almost identical to the figure of physicians who take any type of private insurance!

Alternatively, some retirees may desire to opt out of old-fashioned Medicare (Part A, Part B), also instead, enroll within Medicare Part C, extra commonly well-known when Medicare Advantage plans. Such plans are offered via private insurers, also much provide the whole amount the benefits of old-fashioned Medicare also Medigap policies – also in those days some (i.e., dental benefits, image benefits, etc.) – for subordinate mass premium costs, at the trade-off of a extra restricted network of healthcare providers.

Use COBRA Insurance To Bridge The (Short) Retirement Gap To Age 65

The Consolidated Omnibus Budget Reconciliation Act of 1995, to a greater degree well-known “COBRA”, created another health cover choice for beforehand retirees.

When an single retires from nearly all employers with extra than 20 employees (exceptions request for Federal government employees also certain holy organizations), the employer is required to give the labourer (as well when their mate also vulnerable children) the choice to go on their living health cover coverage, also at the same (full-premium) cost. Upon separation, the employer will give the labourer with a COBRA Election Notice, also a 60-day window within which the retiree also segment of} relations members eligible for reporting necessity produce a judgment in the business of respect to COBRA will begin. (Technically, the 60-day election window begins at the afterwards of the day the labourer separates from service, or their COBRA election sign is provided. However, within practice, employers will not give such a Notice to an [former] labourer up to separation of service occurs.)

The continuation-coverage requirement is not, however, indefinite.

In general, when an single retires – or goes so part-time that they certainly not longer pass for employer-provided health insurance, or just quits or is terminated from their post within widespread – COBRA reporting necessity exist offered via the employer for a minimum of 18 months (employers, at their discretion, can give continuing reporting for longer than prescribed via COBRA). Thus, if a retiree also their mate (if applicable) is/are at smallest 63 ½ when the employee retires, COBRA will previous long sufficient to bridge the gap among termination of work also Medicare.

But while 18-months-of-required-coverage is the widespread COBRA order for employees separating from service, retirees should exist aware of two door key exceptions to that order which can extend the required-coverage period under COBRA further.

Extended 29-month COBRA Health Insurance For A Qualified (Disabled) Beneficiary

One exception to the 18-month order applies when a “qualified beneficiary” is paralysed (as certified via the Social Security Administration via the 60th working day of COBRA coverage). For this purpose, a capable recipient may exist either the labourer separating from service, the employee’s spouse, or the employee’s child.

When applicable, the disability-related annexe to the COBRA reporting window is 11 months. Of note, a disorder via segment of} one capable recipient triggers the 11-month annexe for all qualified beneficiaries, on condition that such persons accompanied by a COBRA-coverage widow of up to 29 months = 18-month “regular” COBRA window + 11-month disability-related COBRA extension.

Example #1: Leslie is 61 years aged also is married to Ben, who is retired also just celebrated his 63rd birthday. For the previous one or two years, both Leslie also Ben keep received health cover although Leslie’s employer.

Leslie, however, has recently come to be paralysed – a disorder certified via the Social Security Administration – also is certainly not longer experienced to work. Upon her termination of employment, Leslie also Ben would exist experienced to go on their living reporting under the “regular” 18-month COBRA window, with the 11-month disability-related extension.

Notably, this would permit Ben to remain on the system from his course years 63 up to he reached his 65th birthday also was entitled to Medicare (at which point, the business can stop Ben’s COBRA window). Additionally, Leslie would exist experienced to stay her living cover for 29 months, at which point, she would also exist eligible for Medicare, expected to her disability.

(Note: In general, workers paralysed earlier to the years of 65 are eligible to get health cover via Medicare. Such reporting is typically sole available, however, after an single has received Social Security disorder benefits for at smallest 24 months. And Social Security disorder benefits don’t begin up to five months after an single is firm to exist disabled. Not coincidentally, the 5-month-Social-Security-disability-benefit waiting period, with the 24 months an single necessity get Social Security disorder benefits earlier to qualifying for disability-related Medicare equals 29 months… the same quantity of while when the “regular” COBRA window upon separation of service with the 11-month long window that applies within the happening of disability!)

COBRA Coverage For Family Members Of Retirees Recently Eligible For Medicare

A following exception to the archetypal 18-month COBRA window that applies upon separation of service – also one which is very appropriate for retirees – is appropriate when the reserved employee became entitled to Medicare smaller than 18 months before the separation of service. As such, this exception much applies when an single retires among 65 also 66 ½.

In such situations, the COBRA window is long up to 36 months after the day the labourer became entitled to Medicare coverage. Of course, since at this point, the retiree can go on Medicare, the retiree, him/herself, won’t miss to employ COBRA continuing coverage. The retiree, however, may keep a younger mate (or a vulnerable child) who motionless needs coverage, also the long COBRA window can help that (those) person(s) bridge segment of} reporting gap.

Example #2: Andy is turn 65 within November 2019 also plans to retire the next month, within December. However, his wife, April, who is covered via Andy’s crowd health cover policy, is sole just history her 62nd birthday, also won’t turn 65 up to July 2022.

Since Andy will exist on top of the years of 65 when he retires, he will employ Medicare when his health insurance. April, on the additional hand, motionless needs health cover reporting to bridge the gap for nearly 3 years up to her Medicare eligibility.

Normally, April’s COBRA continuing reporting would end within June 2021, leaving a abruptly one-year gap among her course living reporting also her Medicare eligibility. However, since Andy became entitled to the Medicare within the 18 months earlier to his retirement, April is eligible for the special 36-month Medicare-related COBRA window. That 36-month period would not end up to December of 2022, which is after April turns 65. Thus, the long Medicare-related window will permit April to bridge the stocked gap among Andy’s separation of service also her enrollment within Medicare.

Primary Benefits Of COBRA Continuation Coverage

COBRA continuing reporting offers several benefits to prospective retirees.

For one thing, “getting” COBRA continuing reporting is simple. There’s certainly not underwriting, it’s guaranteed issue, also reporting can exist terminated at segment of} time.

In situations where separation of service is a predestined event, pre-planning may permit an single sufficient while to appropriately rate a variety of reporting options also reduce the use of this benefit.

In situations where separation of service is unexpected, however, the “comfort” of having a health cover plan with well-known benefits can exist accommodating also allows focus to remain on matters that are much extra critical at the time. If, for instance, an single is terminated from employment, they may turn up it extra valuable to pay out their while keen for a recent post than to pay out while keen for suitable health reporting for themselves also their family. Similarly, if work is compulsory to end expected to illness or injury, the same while may exist best spent focusing on getting better.

Another door key benefit of COBRA continuing reporting is that, since it is the same reporting an single had while employed, there should exist certainly not disruption to ongoing medical care. No while has to exist spent calling doctors to produce certain that they will take the “new” insurance, also certainly not while has to exist spent looking for doctors on a recent plan, since there is certainly not recent plan. In a similar vein, copayments, coinsurance, also additional system features the whole amount remain the same.

Although smaller critical today, gratitude to the Affordable Care Act, COBRA continuing reporting also maintains an individual’s HIPAA eligibility. Under HIPAA, an employer could not exclude a recent employee’s pre-existing state from reporting for extra than a year.

And extra importantly, largely within the circumstances of an beforehand retiree, if an single was HIPAA eligible (had continued [no separate for 63 days or longer] reporting for at smallest 18 months, with the nearly all just gone reporting via a crowd health plan), reporting provided via a recent employers system would begin immediately, also with certainly not restrictions on pre-existing conditions. Furthermore, such HIPAA eligibility guaranteed an single the right, after tiring COBRA continuing coverage, to pay for an individual health cover system straight lacking an employer (and at a while when such plans could otherwise oppose such coverage), virtually making crowd health cover “portable” to single reporting (albeit sole via initial obtaining also tiring COBRA coverage).

The Affordable Care Act certainly not longer allows employers’ health cover plans to oppose reporting for segment of} pre-existing conditions for segment of} period of time. And when discussed within greater fact below, when a result of the same law, single policies purchased via an change are now guaranteed issue also don’t require medical underwriting. Thus, the “portability” benefits of HIPAA are certainly not longer when important when they on one occasion were (before the Affordable Care Act).

The Affordable Care Act, however, has been a source of great governmental controversy, also there keep been several attempts to repeal it within part, when well when within its entirety. In the happening such repeals were in the end effective, HIPAA credibility would likely come to be greatly extra important. Thus, those involved regarding the governmental risks neighbouring the Affordable Care Act should see this issue when evaluating health reporting options.

Cost Of COBRA Continuation Coverage

Given its ease also additional benefits, one might wonder, “Wouldn’t it almost always produce perception to employ COBRA continuing reporting when possible?” Indeed, while that might produce perception for various individuals if they had an unlimited budget, the price of maintaining COBRA continuing reporting is much the “fly within the ointment.”

As noted earlier, when an single elects COBRA continuing coverage, they come to be guilty for the stocked price of the policy. In addition, within nearly all instances, employers are allowed to ask for an extra 2% management fee, bringing the mass price of the plan to 102% of the actual premium. (However, this quantity may exist increased to 50% – making the mass COBRA price 150% of the plan premium – through the extra 11 months within which COBRA reporting is provided on account of a former worker’s disability.)

It is critical to message that the actual premium of COBRA reporting includes segment of} amounts that were being waged via an employer earlier to an employee’s separation of service. Given that the normal employer covers extra than 80% of the price of an single plan also extra than 70% of the price of a relations policy, this extend within price can catch unsuspecting retirees via surprise, also it is much the reason COBRA continuing reporting is turned down. Additionally, COBRA continuing reporting is not ready for the premium credits that are sometimes ready for lower-income taxpayers purchasing reporting via a society change (more on this below).

Example #3: Recently, Jerry was let go from his employer. Prior to his termination, Jerry was paying $300 per month for his relations health insurance, while his employer was picking up the left-over $1,700 balance of the $2,000 monthly premium.

If Jerry decides to go on his living relations reporting via COBRA, his monthly costs will extend from $300 per month to $2,040 = $2,000 x 102%, a nearly 600% extend within Jerry’s actual out-of-pocket price for coverage.

Of course, within various cases the fact is that purchasing health cover on an cover change – since employer reporting is certainly not longer ready – will result within a similarly-substantial price increase, when the leading chauffeur is not that COBRA is “more expensive” however just that it is provided lacking the standard employer-provided premium subsidy. As a result, eligible retirees shouldn’t automatically reject COBRA reporting since of its higher-than-previous cost; instead, it’s needed to balance the price of COBRA to additional ready alternatives at the while of retirement.

“Gaming” The COBRA Rules For Short Coverage Gaps

Given the potential for financial disaster if an single goes lacking healthcare reporting for even a day, it is broadly advisable to stop segment of} gaps within coverage. However, within restricted circumstances, an single can virtually ensure reporting if health services are needed, while avoiding paying for “unnecessary” reporting if such services are not required.

Recall that the COBRA continuing reporting rules require that an single exist particular certainly not smaller than 60 days to produce their COBRA judgment from the afterwards of the day on which reporting is lost, or the day on which they get their COBRA Election Notice. And on one occasion elected, the reporting is appropriate retroactively back to the day the first reporting was terminated (at the end of employment).

Thus, if recent reporting will exist secured via the end of the 60-day COBRA election window (i.e. an single becomes eligible for Medicare, reporting is ready via a spouse’s employer, etc.), an single who does not expect to miss care before the recent reporting is secured can hold off on making the COBRA election accompanied by the hope of avoiding a one or two months of healthcare premiums. If reporting becomes needed within the window, it can exist elected at that time.

Example #4: Ron is arrangement to retire from his employer on December 31, 2019, at which point his employer-provided health reporting will terminate. Ron, however, will turn 65 on March 25, 2020, in this way making him eligible for Medicare when of the initial of that month.

If Ron wants to, he can “game” the COBRA rules to potentially stop buying health cover for January also February of 2020. Given that Ron has certainly not smaller than 60 days from the day he loses reporting to produce a COBRA decision, if Ron has certainly not immediate healthcare needs, he can just “sit tight” also work zero through the two months among his separation of service at the end of 2019 also when his Medicare reporting begins at the opening of March, 2020.

Suppose, however, that on February 15, Ron has shortness of wind also goes to the infirmary for evaluation. At that time, he can communication his former employer to choose COBRA continuing reporting also minimize his out-of-pocket expenses for the infirmary go to see (though while the reporting itself would exist retroactive backwards to Ron’s termination, that also method Ron would owe COBRA premiums for both January also February 2020 if he finished out needing to produce the COBRA election).

(Note: While COBRA rules sole request to employers with 20 or extra persons, many states keep similar requirements, via what are well-known when “Mini-COBRA” laws. Thus, those separating from service from smaller employers should test to see what options are ready to them under nation law, largely since Mini-COBRA rules be different dramatically from nation to state.)

Convert Group Health Insurance To An Individual Plan

An extra choice for some retirees is to “convert” their crowd health cover plan into their personal single health cover plan.

The power to convert a crowd plan to an single plan is an choice that can exist provided via a plan, however it is not required. However, if such an choice is ready to a party upon separation of service (as an alternative to COBRA continuing coverage), the same choice necessity also exist made ready at the end of the COBRA continuation-coverage window (if COBRA reporting was elected also maintained up to that time).

Unlike COBRA continuing coverage, though, the language of a conversion plan work not keep to exist the same when the “old” policy. As such, premiums for such policies may exist higher, and/or the plan may give a subordinate standard of coverage. As such, conversion options necessity exist evaluated on a case-by-case basis.

Finally, it’s critical to message that while COBRA continuing maintains an individual’s HIPAA-eligibility status, conversion reporting is single fair coverage. Thus, it does not retain an individual’s HIPAA eligibility. Although far smaller critical within the post-Affordable Care Act world when health cover policies keep come to be guaranteed issue via health cover exchanges, HIPAA eligibility continues to give individuals purchasing single reporting greater charge than is otherwise ready via nation law.

Purchase An Individual Policy (On A Public Healthcare Exchange)

Another choice for beforehand retirees looking for healthcare reporting is to purchase a health cover plan via a nation health cover exchange.

This choice is much the best choice for retirees who either:

- Find that their COBRA continuing and/or conversion plan options are also expensive to retain (or that they would prefer smaller robust, however smaller expensive coverage).

- Have exhausted their COBRA continuing reporting window also are motionless not eligible to enroll within Medicare.

- Are moving to another nation after retiring, also one or two (or maybe even no) doctors within the recent point will take the living COBRA continuing reporting insurance.

- Can get premium assistance rate credit subsidies for their health cover when a result of “low” income.

Public health cover exchanges were created via the Affordable Care Act (commonly well-known when ACA or “Obamacare”) also serve when a marketplace for persons seeking health cover coverage. Each nation has either its personal exchange, uses the one created via the Federal government, or uses some good of cross approach. Functionally, though, the end result is the same: individuals get a series of health cover options within their nation however necessity pay for health cover from the nation within which they retain their lasting address. (If that nation of residence changes, thus a lot their coverage.)

Of decisive significance for various retirees is that, since 2014, the Affordable Care Act has prescribed that the whole amount major medical cover policies exist issued on a guaranteed basis. Thus, an single can certainly not longer exist denied for a pre-existing condition. And to that end, the often-arduous medical underwriting means that applied within the pre-ACA era is also certainly not longer applicable. In additional words, an beforehand retiree is assured – similar to COBRA reporting – of being experienced to transition from employer-provided health cover to a private cover system via an cover exchange, regardless of segment of} health conditions.

But while a retiree can’t exist denied reporting for a pre-existing medical condition, they cannot just pay for reporting via an change whenever they want. Rather, reporting can only exist purchased through an enrollment period. In general, retirees who be beaten employer-provided health reporting also desire to cover themselves via an exchange-purchased plan should get reporting through their Special Enrollment Period. The Special Enrollment Period begins when the employer reporting is terminated also ends 60 days later.

If reporting is not purchased through this time, it is broadly needed to stay up to the next Open Enrollment Period (which runs from the opening of November to mid-December every year, accompanied by reporting taking effect at the opening of the subsequent year). However, this could leave a retiree seriously revealed to healthcare costs incurred earlier to the begin of that coverage.

Example #5: Chris is an exceptionally well single who retired on February 10, 2019, at the years of 63. Given his exceptional health also the Tax Cuts also Jobs Act’s repeal of the single order efficient opening 2019, Chris certain to “roll the dice” also stay up to 65 to enroll within Medicare to keep health cover coverage.

Unfortunately for Chris, within August of 2019, he begins to be in pain from severe burning an unexplained weight loss. Eventually, Chris “gives in” also gets checked out. As it turns out, he has Hodgkin’s Lymphoma also necessity begin medical care immediately.

In this situation, Chris would sole exist experienced to enroll within health cover reporting through the next Open Enrollment Period, which doesn’t open up to November 1, and reporting wouldn’t begin up to January 1, 2020! Thus, Chris would exist guilty for the stocked price of his medical care from August up to next January (which could without a doubt bankrupt him, even if he had significant savings!)

Cost Of Exchange-Purchased Health Insurance Policies

The price of an cover plan purchased via an change can be different dramatically based on a figure of factors, however somewhat ironically, an individual’s health is not one of them! Rather, under Federal law, the only five factors that cover companies can employ (unless the nation uses even fewer factors) when establishing premiums are:

- Age

- Location

- Tobacco use

- Individual reporting vs. reporting for an single also a mate and/or dependents

- Plan grouping (i.e. Bronze, Silver, Gold, Platinum, also Catastrophic)

Perhaps not surprisingly, health cover purchased via an change for beforehand retirees can exist rather expensive. After all, healthcare needs be likely to extend when an single ages.

As noted earlier, the normal price of a Silver Plan purchased via an change for a 64-year-old within 2019 is $1,123. But that’s just the average, also the actual cost of cover can be different considerably from point to location. For example, a Silver Plan will price a 64-year-old work within Lincoln, Nebraska regarding $1,758 per month. That’s extra than 50% higher than the nationwide average! Meanwhile, a Silver Plan for the same 64-year-old work within Indianapolis, Indiana would price “just” $885 per month.

In a minute figure of states, though, health cover for beforehand retirees is dramatically cheaper than the nationwide average, gratitude to what’s well-known when Community Ratings. Most states permit insurers to ask for extra to give health cover to an older being than to a younger person. But within a minute handful of states, insurers are prescribed to employ Community Rating, within which the whole amount persons within a geographic region are charged the same for the same insurance, regardless of their age.

As one might imagine, Community Rating systems result within younger individuals having health cover costs that are higher compared to individuals of the same years within other, non-Community Ratings-based locales. But while it may come at the charge of younger persons, this is broadly a boon for older individuals who miss to pay for health cover via an exchange, whose policies are not increased in price for their years (as they would exist within additional areas).

For example, within New York, New York – an region in the business of one of the highest costs of work within the state – the average monthly premium waged via a 64-year-old single purchasing a Silver Plan within 2019 is just $585! And that $585 premium is accurately the same premium that would exist waged via a 24-year-old single within the same place!

Subsidizing Health Insurance Exchange Coverage With Premium Assistance Tax Credits

After separating from service, some retirees will experience a dramatic lowering within income. In such situations, individuals may turn up themselves eligible to get a Premium Assistance Tax Credit – i.e., an cover premium subsidy – to help them pay for the price of their health insurance.

In order to pass for a Premium Assistance Tax Credit (PATC), an single necessity pay for health cover (other than catastrophic insurance) via an change (thus, COBRA reporting or a converted crowd plan does not qualify), and broadly meet the next requirements:

- Household revenue among 100% also 400% of the Federal Poverty Level for the relations size ($12,140 to $48,560 for a single single within the continental U.S. through 2019, or $$16,460 to $65,840 for a married couple)

- Cannot exist claimed when a vulnerable via someone else

- Cannot exist eligible for reporting via a government program (i.e., Medicare, Tricare, CHIP, Medicaid) or exist experienced to pay for fair reporting (less than 9.86% of home revenue for employee’s price of employee’s reporting for 2019) via an employer-sponsored system of minimum quality (actuarial equal of a Bronze plan, or higher).

- Cannot file married-separate

- Be a U.S. citizen or lawful resident

When eligible, the PATC an single receives is calculated using a involved formula that is based on comparing the individual’s home revenue to the price for the second-lowest-priced Silver Plan ready within the state. However, while the cost of the second-lowest-priced Silver Plan is the benchmark to affect the rate credit itself, a retiree can pick to pay for segment of} system they desire (and employ whatever credit is ready towards the selected plan).

Purchasing a Bronze Plan, for instance, might permit a low-income retiree to completely offset the price of their health cover with the premium they received. Meanwhile, if a retiree purchased a Platinum Plan, they would almost certainly keep to foot a significant share of the rate via savings or some additional means.

The price of healthcare is one of the nearly all hotly debated topics within the politisphere, when well when one of the nearly all concerning for retirees.

Fortunately, for individuals reserved at 65 or later, the challenge of securing cost-efficient also efficient health cover is broadly minimized gratitude to the readiness of Medicare.

For younger retirees, however, securing quality healthcare reporting can exist problematic, largely for those with a restricted budget. Options contain COBRA continuing coverage, converting a crowd health system to single coverage, also purchasing cover via their state-approved exchange. Each of these options provides its personal unique benefits also drawbacks, in this way further complicating matters for various individuals through a period of while within which there is before massive change also complication.

In general, the best choice for retirees, when available, is to “hop onto” Medicare. When that isn’t an option, the enquiry is generally, “Would I rather stay my course coverage, via COBRA, for when long when possible, or should I just get an single reporting via an exchange?” Like various issues, this just becomes a price vs. benefit analysis.

Will door key doctors take the recent exchange-purchased insurance? How expensive is the COBRA continuing reporting within comparison to the exchange-purchased policy? Would Premium Assistance Tax Credits exist ready for an exchange-purchased policy? These are the types of questions retirees necessity ask themselves, also answer, within order to produce a noise decision.

For some couples losing employer-provided health benefits, two individual courses of action may exist best, creating until now another difficulty when what was one time “standard home coverage” is split. This can leave every mate accompanied by their personal plan (e.g., Medicare for one also an exchange-purchased plan for the other), perfect with their personal specific deductibles, coinsurance, also list of physicians accepting such coverages. For others, the “best” course may exist a mix of several options, such when COBRA continuing coverage, followed via the pay for of an change plan when COBRA expires, also ultimately Medicare at years 65.

begitulah pembahasan mengenai Figuring Out The "Best" Healthcare Option For Early Retirees semoga artikel ini bermanfaat terima kasih

Artikel ini diposting pada kategori the best health insurance coverage, find the best health insurance coverage, best health insurance coverage canada, , tanggal 21-08-2019, di kutip dari https://www.kitces.com/blog/best-healthcare-early-retirement-medicare-cobra-aca-exchange/

No comments:

Post a Comment